A checking account and Monero both let you hold and move money, but they work in almost opposite ways. One lives inside the banking system and is built for convenience, reversibility, and integration. The other lives outside of it and is built for privacy, finality, and control. Understanding the difference — especially how bank payments and ACH actually work — is the key to using each one where it shines.

How a checking account works

When you open a checking account, the bank holds your money for you and gives you tools to move it: a debit card, checks, wire transfers, and — the workhorse of U.S. banking — ACH transfers. Your balance is an entry in the bank's database, insured by the FDIC up to $250,000, and the bank acts as the middleman for every transaction. That middleman role is exactly what makes a checking account so convenient and what gives it its limits.

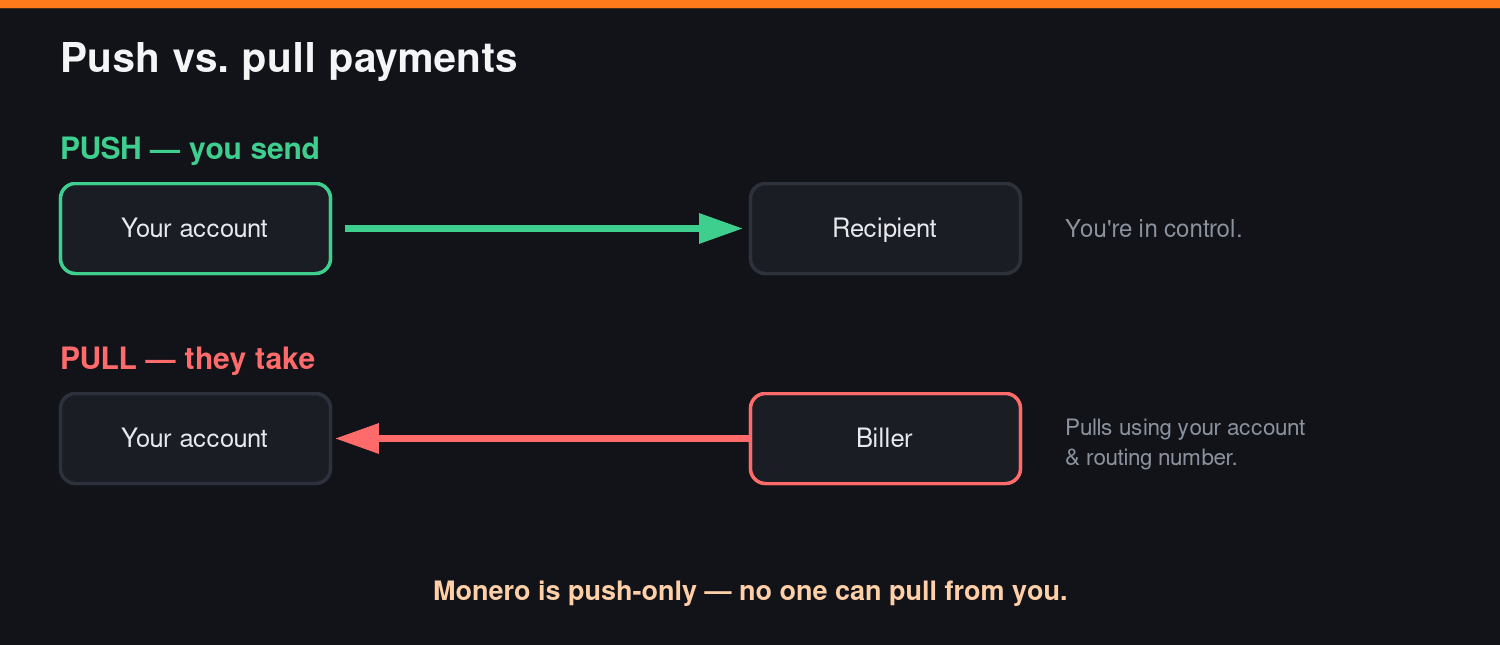

How ACH works: push vs. pull

ACH stands for Automated Clearing House — the batch network that moves money between U.S. bank accounts. Direct deposit, autopay, and most “bank transfer” payments run on ACH. There are two directions, and the difference matters:

- Push (ACH credit). You tell your bank to send money out — paying a bill through your bank's bill-pay, or your employer sending your paycheck. You control it, and money leaves only when you say so.

- Pull (ACH debit). Someone else initiates the transfer and pulls money from your account — a subscription, a utility on autopay, or a lender collecting a payment. To allow it, you hand over your account and routing numbers, which is why those numbers are effectively a key to your account.

ACH is cheap (usually free for consumers), but it's slow and reversible: transfers settle in one to three business days — nothing clears on weekends or holidays — and payments can be returned or disputed for a window afterward. That reversibility is a feature when you're scammed or double-charged, and a headache when you're the one waiting to be sure a payment is final.

How Monero works for payments

Monero flips almost every one of those properties. There's no bank and no account number. You hold your own keys, and you send money directly, peer to peer. Monero is push-only: you can send, but no one can pull from you, because there's no account for anyone to debit. Payments are final — once confirmed (usually within a few minutes), they can't be reversed or charged back. And they're private by default: the amounts, sender, and receiver are hidden on the network. The fee is a flat few cents (around $0.04) no matter how much you send.

Fees compared

- Checking account. Consumer ACH is usually free, but the fine print adds up: overdraft fees, wire fees ($15–$35+), foreign-transaction fees, minimum-balance fees, and returned-payment fees. Sending money abroad is slow and expensive.

- Monero. A single flat network fee of roughly $0.04, whether you send $5 or $50,000, anywhere in the world. The main cost is converting to and from your local currency on an exchange.

What each can and can't do

A checking account can receive a direct-deposit paycheck, put bills on autopay, write checks, tap a debit card at almost any store, pull cash from an ATM, dispute fraud and reverse mistakes, and plug into the entire U.S. financial system. It can't be private (your bank — and, with a request, the government — sees every transaction), can't be censorship-resistant (accounts can be frozen, garnished, or closed), and can't give you truly final settlement.

Monero can send value privately, finally, and permissionlessly to anyone in the world, held entirely by you, with no account for anyone to pull from. It can't do autopay or pulls, can't be reversed if you're scammed or fat-finger an address, isn't FDIC-insured, can't be spent directly at most mainstream stores, can't receive a normal paycheck, and can't be recovered if you lose your keys.

The limits and access a checking account has

Because a bank sits in the middle, a checking account comes with strings: daily and per-transaction ACH limits, holds on deposits before funds are available, settlement only on business days, mandatory identity verification (KYC), and the reality that the account can be frozen, garnished, or closed by the bank or a court. In exchange, you get insurance, disputes, and seamless integration with billers, employers, and stores. Monero has none of those strings — and none of those protections.

Which is best for what

- Use a checking account for: receiving your paycheck, paying U.S. bills, autopay, everyday debit-card spending, ATM cash, and anytime you value reversibility, disputes, and FDIC insurance.

- Use Monero for: private payments, saving value outside the banking system, sending money across borders cheaply, paying merchants who accept XMR, and any situation where finality and control matter more than the ability to reverse.

Pros and cons at a glance

Checking account — pros: convenient, reversible, insured, integrated, supports pull/autopay and direct deposit. Cons: not private, can be frozen, slow settlement, fees on the edges, permissioned.

Monero — pros: private, final, self-custodied, borderless, tiny flat fee, no pull risk. Cons: irreversible, not insured, no autopay, limited acceptance, you alone are responsible for your keys.

How to use both for the best outcome

You don't have to choose. The smartest approach for most people is to use each tool for what it's good at: keep a checking account as your bridge to the everyday world — paycheck in, bills out — and use Monero for privacy, for savings you want outside the system, and for sending value where banks are slow or unwelcome.

The link between the two is an exchange. You fund the exchange from your checking account over ACH, buy Monero, and withdraw it to your own wallet. To cash back out, you send Monero to the exchange, sell it, and ACH the dollars back to your bank. For that on-ramp and off-ramp, a well-established, ACH-friendly exchange like Kraken is a solid choice — you can link your bank for easy ACH funding to buy Monero, and later sell it back to your checking account the same way. (Coin availability varies by region, so check what's offered where you are.)

The bottom line: a checking account is the better tool for plugging into the mainstream economy, and Monero is the better tool for privacy, finality, and control. Use ACH and your bank for the rails, use Monero for the money you want to truly own — and an exchange like Kraken to move smoothly between them.