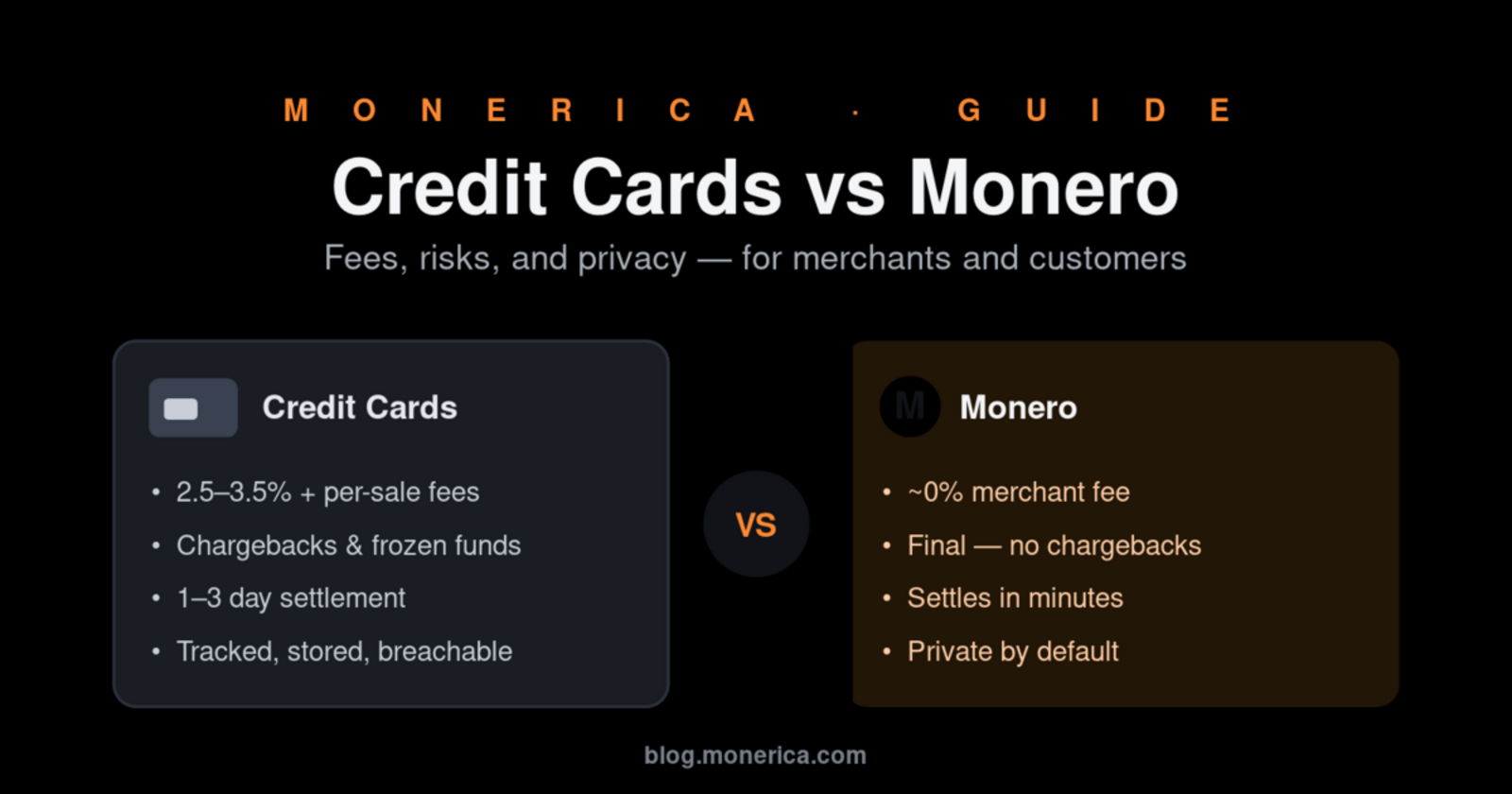

Every payment is a trade-off. When a customer taps a credit card or sends Monero, they're choosing a different mix of fees, privacy, risk, and control — and so is the merchant on the other side. This guide walks through those differences in detail, from both the merchant's and the customer's point of view, so you can see exactly what each side gains and gives up.

The short version

| Credit cards | Monero (XMR) | |

|---|---|---|

| Merchant fee per sale | ~1.5%–3.5% + $0.10–$0.30, plus gateway & monthly fees | Network fee only (cents), paid by the sender; ~0% to the merchant |

| Chargebacks | Yes — funds can be pulled back for months | None — payments are final once confirmed |

| Settlement time | 1–3 business days (sometimes weeks in reserve) | Minutes; funds are yours immediately |

| Who holds the money | Banks & processors, who can freeze or terminate accounts | You do (self-custody), unless you choose a custodian |

| Privacy | Card number, identity, and purchase history recorded and shareable | Amounts, sender, and receiver hidden by default |

| Reversibility for the buyer | Strong — dispute a charge and often win | None — the buyer must trust the merchant |

| Access | Requires a bank/credit approval; can be denied | Permissionless — anyone with a wallet |

For the merchant

Fees: the part that quietly eats your margin

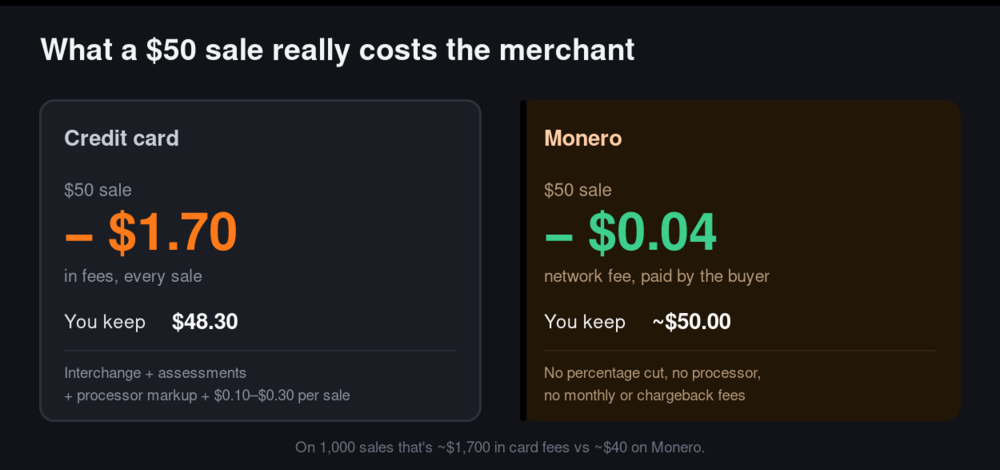

Card acceptance is rarely a single number. A typical online sale is charged an interchange fee (set by the card networks, usually ~1.5%–2.5% for consumer cards, higher for rewards and business cards), a small network assessment, and a processor markup — landing most merchants around 2.5%–3.5% plus $0.10–$0.30 per transaction. On top of that there are often monthly gateway fees, statement fees, PCI-compliance fees, and minimums. Sell a $50 item and you may keep ~$48.30; sell a thousand of them and you've handed over $1,700+.

With Monero, the buyer pays a network fee of just a few cents (around $0.04 today) to the miners, not to you. There is no percentage cut and no intermediary invoice. If you use a self-hosted processor like BTCPay Server, your cost is essentially your server. If you use a hosted payment button, you might pay a small flat fee — but nothing like a 3% card rate. For high-volume or thin-margin sellers, that difference is the whole game.

Chargebacks and fraud: the risk cards put on the seller

With cards, the merchant carries the fraud risk. A stolen card, a "friendly fraud" dispute ("I never got it"), or a genuine mistake can trigger a chargeback — the bank claws the money back, often months later, and typically adds a $15–$100 chargeback fee whether or not you win. Lose too many and processors raise your rates or drop you entirely. You can end up shipping a product and losing the money and paying a penalty.

Monero payments are final. Once the transaction confirms on-chain, it cannot be reversed by the buyer, a bank, or anyone else. That removes chargeback fraud completely — a major reason digital-goods and high-risk sellers accept it. The flip side is that finality shifts trust onto the buyer, so a reputable merchant should be clear about refunds and support (more on that below).

Settlement and cash flow

Card funds usually land in your bank in 1–3 business days, and "high-risk" merchants may face rolling reserves where a processor holds a slice of revenue for weeks or months as a chargeback buffer. Monero settles in minutes, and the money is yours the moment it confirms — no reserve, no holdback, no waiting on a Friday-to-Monday gap.

Account risk and control

A card merchant account is permission you're granted — and can lose. Processors routinely freeze funds or terminate accounts for "prohibited" or "high-risk" categories, sudden volume spikes, or too many disputes, sometimes with little warning. With Monero you self-custody: the funds arrive in your wallet and no third party can freeze or reverse them. That independence is powerful, but it also means you are responsible for securing keys and backups — there's no support line to reset a lost seed phrase.

Compliance and data liability

Accepting cards means touching cardholder data, which pulls you into PCI-DSS scope and makes you a target: a breach of stored card data can mean fines and lawsuits. Monero payments carry no card numbers and no customer identity to leak, which shrinks both your compliance burden and your breach liability.

For the customer

What it costs you

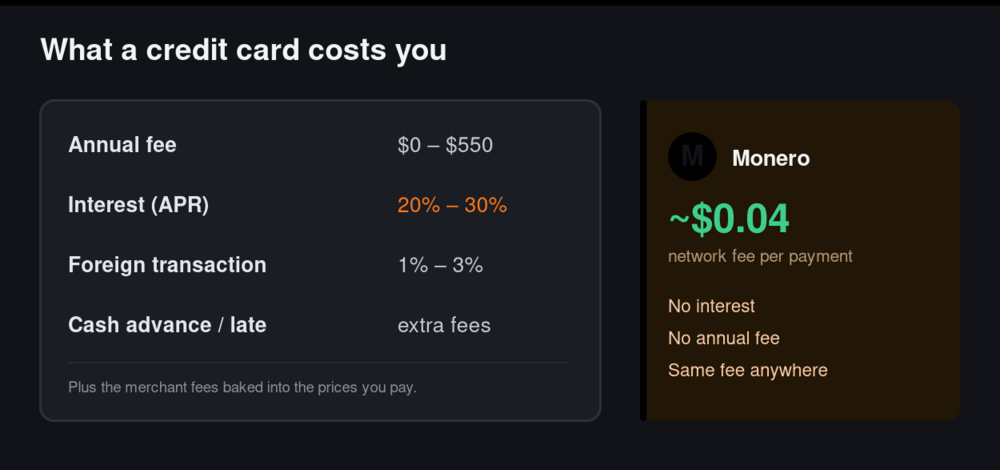

Cards feel free at the register, but the costs are real: annual fees on many rewards cards, interest (often 20%–30% APR) on any balance you carry, foreign-transaction fees of ~1%–3% abroad, cash-advance fees, and late fees. Rewards are partly funded by the merchant fees baked into prices everyone pays. Paying with Monero costs you only the small network fee — currently about $0.04 — with no interest, no annual fee, and the same fee whether you're buying at home or across the world.

Privacy: who sees what you buy

This is the sharpest difference. A card transaction records your identity, the merchant, the amount, the time, and your location — data that banks and networks retain, analyze, and can share or sell, and that gets exposed in the regular drumbeat of data breaches. Monero is private by default: ring signatures, stealth addresses, and confidential amounts hide the sender, receiver, and value on-chain. Your purchase isn't added to a profile, and there's no card number sitting in a database waiting to leak.

Fraud, liability, and reversibility

Cards give buyers strong protection: most offer zero-liability for fraud and let you dispute a charge if a merchant fails to deliver — a real safety net, though it can mean frozen cards and weeks of hassle to resolve. Monero has no chargebacks, which cuts both ways: no one can reverse a payment you didn't authorize because you hold the keys (so there's nothing to steal remotely from a "card number"), but if you send to a scam or the wrong address, there's no bank to undo it. It rewards dealing with reputable sellers and double-checking addresses.

Access

A credit card requires a bank relationship and approval — a credit check, an ID, sometimes a rejection. Monero is permissionless: anyone with a wallet can send and receive, with no gatekeeper, credit score, or geographic exclusion. For the underbanked or anyone who's been de-platformed, that access is the point.

The core differences, distilled

- Reversible vs final. Cards can be pulled back (protecting buyers, exposing merchants); Monero is final (protecting merchants, requiring buyer trust).

- Surveilled vs private. Cards create a permanent, identifiable record; Monero hides amounts and parties by default.

- Intermediated vs peer-to-peer. Cards route through banks and processors who take a cut and set the rules; Monero moves directly, wallet to wallet.

- Custodial vs self-custodial. With cards, institutions hold and can freeze funds; with Monero, you hold them — and the responsibility that comes with it.

- Percentage fees vs flat network fees. Card costs scale with price and volume; Monero's fee is a few cents regardless of amount.

So which is "better"?

Neither is universally better — they optimize for different things. Cards buy the customer convenience and dispute protection, and buy the merchant reach and familiarity, in exchange for fees, surveillance, and the ever-present chargeback risk. Monero gives the merchant near-zero fees, instant final settlement, and no frozen accounts, and gives the customer privacy, low cost, and open access, in exchange for giving up the reversibility safety net.

For many sellers — especially privacy-respecting, digital-goods, or thin-margin businesses — accepting Monero alongside cards captures the best of both: shoppers who want protection can still use a card, while those who value privacy and lower prices can pay with XMR and skip the middlemen entirely. If you're a merchant weighing it up, a self-hosted processor keeps your costs and your custody in your own hands; if you're a shopper, Monero is simply the most private, lowest-cost way to pay a business that accepts it.

Want to find businesses that already take Monero? Browse the Monerica directory, or if you're setting up acceptance yourself, see our guide to running BTCPay Server on a private host.